How public markets and venture financing differ.

Christopher Koch, Deputy Chief Financial Officer of Freelancer Limited, gave his keynote presentation about the Valuation of Technology Companies in Public Markets at SydStart 2015. This talk was at the start of a heated month of debate in global public markets on the challenges of privately held ‘unicorns’ going public, and just ahead of some key investors’ write-downs of privately held ‘unicorns’, along with the eventful Square and Match IPOs.

Public Markets

Public markets are very different to venture financing. Public markets are fully diluted, fully transparent, operate in real-time, and come with onerous continuous disclosure obligations. There is also no ‘liquidation preference’ style of sequential series’ of investments each with different interacting and often cumulative rights, each dependent on the valuation of future financing rounds or other outcomes. Public markets are ‘pari passu’ where, in almost all cases, each ordinary share is equal in rights and interests.

WATCH CHRIS’ FULL KEYNOTE WITH AN ALL ACCESS DIGITAL PASS.

Terminology

To better understand the valuation trends of technology companies, Christopher debunked a range of acronyms and terminology on four key points.

How do public markets look at earnings? They look at earnings in broadly two ways:

1. Profit or NPAT (Net Profit After Tax) — the ‘bottom line’ or all the profits retained after paying interest and taxes – fully ‘bakes’ a capital structure into the measure of profit

2. EBITDA (Earnings Before Interest, Tax, Depreciation and Amortisation) — a measure of earnings that is capital structure free, removing financing flows such as interest, non-cash measures (depreciation and amortisation), and taxes (which are also themselves a function of capital structure); this is also a measure of a company’s ability to service its capital structure on a cash basis

Those two earning metrics — one that ‘bakes’ your capital structure and the one that does not — also tie into the two broad ways public markets express the value of a business:

1. Equity (typically market capitalization of fully paid ordinary shares) — the residual value of the enterprise to its owners’

2. Enterprise value — the value of this equity plus the value of any debt (less any cash). Enterprise value becomes an important concept when you have debt in your capital structure and you need to think about the whole value of the business — to buy a business, you would have to ‘buy’ the equity and ‘buy’ the debt in the sense that you are taking this debt on. Similarly, ‘buying’ cash makes no sense… so it’s just netted off.

NPAT is the profit measure typically used in connection with equity – as it is the final measure of earnings after interest on any debt is paid for, and taxes are paid, effectively the return to rump equity holders. EBIT is typically paired with enterprise value — as it is the measure of cash earnings independent of any capital structure, which can be used to service the whole capital structure (debt and then equity).

Public markets often use ‘multiples’ when discussing valuation. These are deceptively simple — just the ratio of a valuation metric to an earnings metric. Ratios are used to compare companies of different sizes. It’s that simple. That’s why EV is paired with EBIT or EBITDA for multiples (like EV/EBIT and EV/EBITDA), as it matches capital structure free flows with the broadest definition of valuation, incorporating both equity and debt. NPAT is then typically paired with equity (P/E, which is price/earnings, is just a per share way of expressing market capitalisation / NPAT), as it is rump earnings and rump equity or interest in the company.

It’s just a relativity from one to another — and size cancels out. This way, you can compare the P/E of Apple to the P/E of SEEK, when you want to for benchmarking and other things like that.

Key Drivers of Public Market Valuation

In public market valuation, financial metrics (revenue, earnings, cash flow and conversion) become very important considerations for anyone valuing a business and its relative risks. Key elements of this are any outlook statements (your forecast or guidance), MD&A (management, discussion, and analysis of financial reports), and analyst consensus (how the investment community at large thinks about your business based on reports and financial analysis published by independent research analysts).

What Drives Exceptional Public Market Valuation

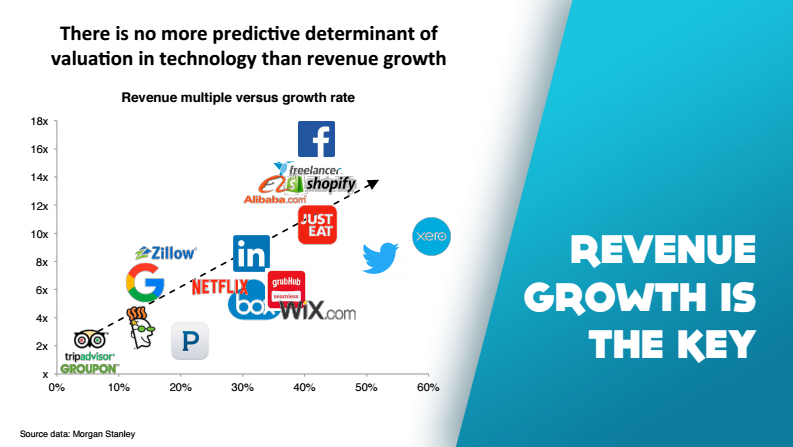

The most significant driver of valuation in a technology business is revenue growth. “If you want a really punchy trading multiple, revenue growth is the single most influential factor to actually get that valuation for you,” Christopher said.

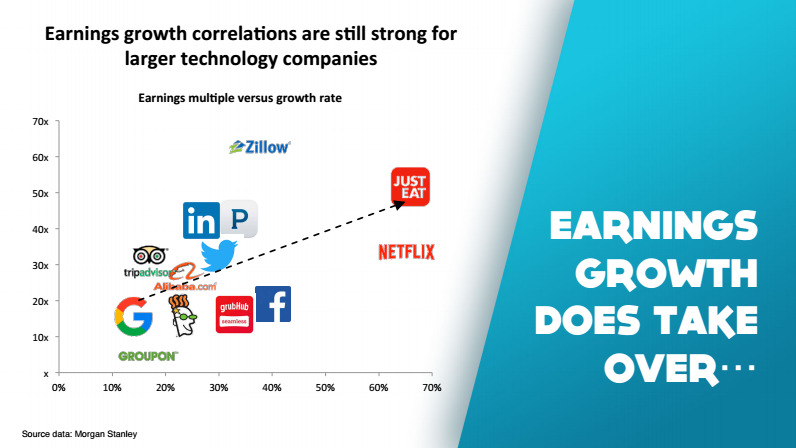

When your company is larger and you have earnings, earnings multiples become relevant as well.

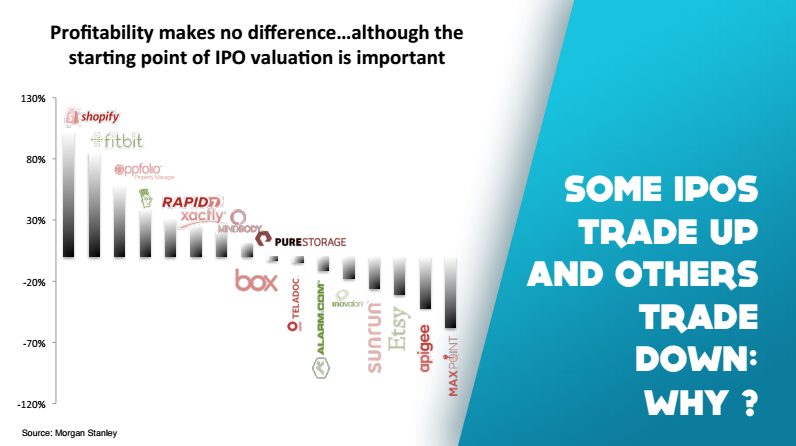

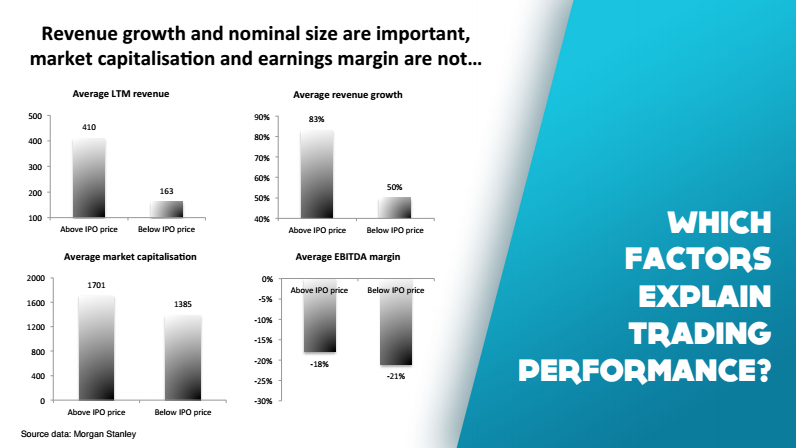

But, why do some deals trade up and some trade down? Ultimately how tightly priced a deal is at the time it is printed is impactful here, but it turns out other factors are much more explanatory. Interestingly, check out the chart below — red logos are loss making businesses, green logos are profitable. No difference, right?

If you look into the data, it turns out that the size of your revenue line in nominal dollar terms and revenue growth make a huge difference, not the absolute size of your business nor your earnings margin (noting both earnings margins are negative on the chart on the bottom right hand side of this chart).

Is revenue really everything? Yes. But investors want to know whether at some point in the future, you can monetize all the revenue you are growing. Christopher shared that at Freelancer, they have articulated very clearly that right now, they are running a business flat at the earnings line — no profit, no loss. Helpfully, as a marketplace business Freelancer is cash flow positive even at a small EBITDA loss.

Unicorns

Right now in technology, there are more ‘unicorns’ than ever before — privately held (unlisted) businesses with massive theoretical or implied valuations. For example, Uber recently raised US$1 billion at the margin, on a theoretical and extrapolated ‘valuation’ of over US$70 billion.This all gets back to the fundamental difference between heavily structured ‘liquidation preference’ style venture capital valuations and the fully diluted and transparent valuations in public markets. “It’s very rare for an IPO to be hundred percent selldown. Basically it doesn’t happen. An IPO might be 20% to 50% of the value of the company at one point in time, but then again, every day that trades so it’s changing every second and becomes typically very representative of a fundamental or more underlying valuation” said Christopher.

The challenge here is to assess whether these businesses can hold or sustain these valuations in a public market context. This summarises all of the things we have discussed so far today. Taking a point reference (say, raising $1 billion for Uber) and extrapolating it to a theoretical valuation of $70 billion is easy enough. It’s static, it doesn’t change — it may even be heavily reliant on the term sheet features (such as ratchets and liquidation preference structures) that are unobservable.

Public markets are very different. Shares can trade every day, every second. These valuations are less theoretical, and tested continuously. Also, there are no hidden term sheets. The nature of transparent disclosure in public markets means that every share is equal, and very little information is kept from these markets.

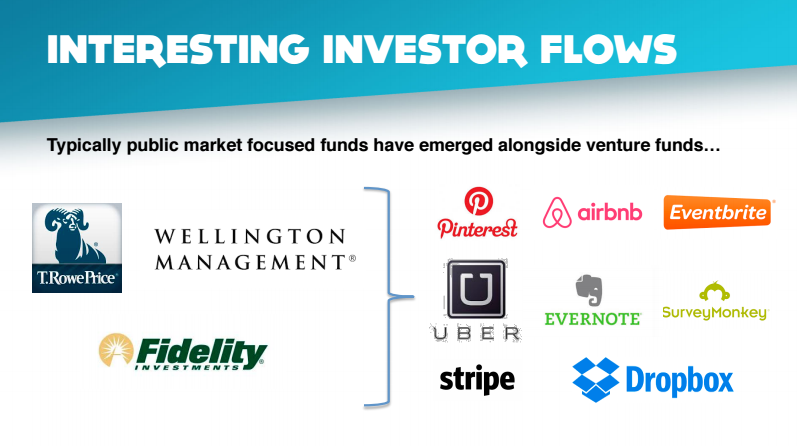

So, how do these businesses make this transition and will the valuations be supported? One very interesting thing has happened very quietly in the landscape and behind the scenes here. Some of the world’s biggest, smartest and historically best public market investment funds — the kind that many of us would hold superannuation or 401(k) style savings accounts with and have invest on our behalf — are invested in these unicorns. Check out funds like T Rowe, Wellington and Fidelity:

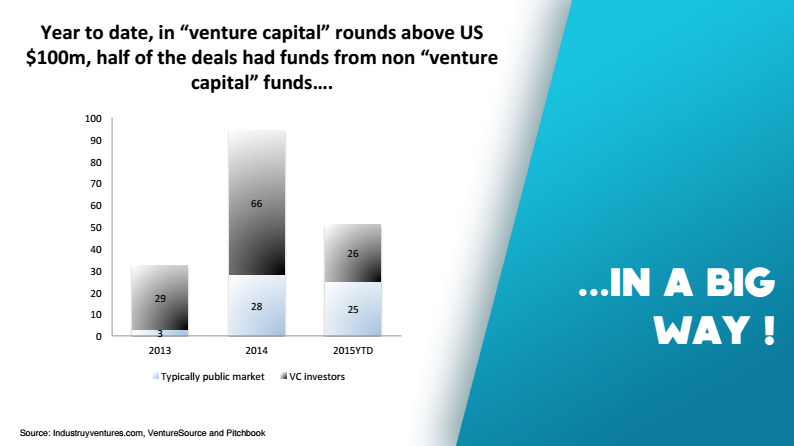

In fact, half of the deals this year have had some of these typically public market investors make significant investments:

This is significant for many reasons. Just to start with, these funds have different disclosure obligations compared to venture capital funds. They publicly report regularly and write-downs or write-ups in these investments could be transparent. But also, they may have more of an incentive to continue to provide financial support and fund future rounds of investment even at or beyond IPO, given their material investments.

Ultimately, this change in valuation perspective from private to public markets may fundamentally revalue these businesses:

Preparation for Listing a Startup

If part of your future plan is to list a startup, you need to think ahead.

First, when you bring a business to capital markets, make sure you’re counting everything correctly. You have to publish a three-year historical report at IPO in most jurisdictions. That historical period, whether it represents the majority or just the recent handful of periods of your financial reporting, becomes the most reviewed historical perspective on your business by investors. Next, how do you want your business financials to look like (your profits and losses in particular)?

Christopher suggested that it’s much more compelling to present different phases and different narratives on how you built your business. This might be growing at a loss making or cashflow negative rate, or, for example, the current stage at Freelancer of exceptional growth but at effectively flat on the P&L, with positive operating cashflow. Swinging to profitability or entering different phases of growth and maturity in different aspects of the business — all of these need a succinct, compelling explanatory narrative.

Watch Chris’ full keynote with an All Access Digital Pass.

Christopher spent nearly a decade as a merchant banker, finishing as a Director at Swiss investment bank UBS. He worked on $35 billion of transactions including listings on the Australian Securities Exchange (ASX) and the New York Stock Exchange (NYSE), on matters across Australia, Hong Kong, mainland China, Tokyo, London, Europe and the United States.

Christopher completed his masters in finance at INSEAD (France and Singapore campuses), and read economics and law with first class honours at the University of Adelaide. His career started in government where he worked for His Excellency The Honourable Alexander Downer AC during the Howard government.